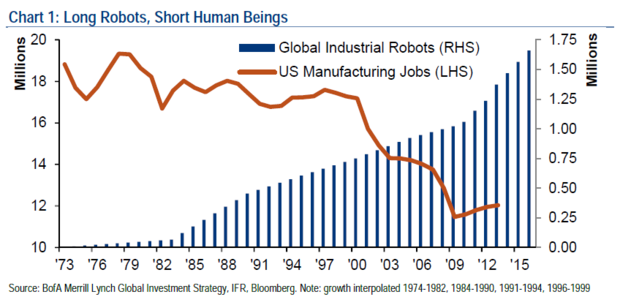

The below chart from a indeterminate Bank of America report seems to be making the rounds today, interesting not just for the data, (which has two problems, one, it is kind of obvious to anyone watching the American economy over the last 30 years or so that manufacturing has been on the decline; and two, that it attempts to compare US manufacturing employment to Global industrial robot production).

But still it is kind of a fun chart, not the least of which for its title, Long Robots, Short Human Beings. Clever Bank of America!

Except it might not be all the funny, even for the highly educated, well-paid types of folks that are likely working at Bank of America and would have put together a chart like this.

The robots are not just going to be satisfied and content with the boring, industrial, just another machine in the machine type factory jobs that are the main subject of this chart.

No, Mr. and Ms. Bank of America hotshot. The robots are probably coming for you too. Just a couple of examples to consider.

From the Abnormal Returns blog - 'The rising challenge of robo-advisors'

It has been my hypothesis for some time now that the rise of the exchange-traded fund, or to be more specific the ultra low-cost, indexed ETF has made possible the growing wave of online, algorithmic asset managers (or robo-advisors).* In short, this abundance of low-cost portfolio building blocks available from a host of fund sponsors makes low-fee online portfolios possible. A couple of years ago I noted that most investors’ portfolio needs are not all that unique. Therefore algorithms could handle the bulk, but not all of their needs.

Or perhaps the disruption to the Bank's models will come from IBM Watson. The below is taken from the 'Watson at Work' section of IBM's site:

Watson is being designed as the ultimate financial services assistant, capable of performing deep content analysis and evidence-based reasoning to accelerate and improve decisions, reduce operational costs, and optimize outcomes.

In a bank, an advisor can use Watson to make better recommendations for financial products to customers based on comprehensive analysis of market conditions, the client's past decisions, recent life events, and available offerings.

The ability to take context into account during the hypothesis generation and scoring phases of the processing pipeline allows Watson to address these complex financial services problems and assist financial services professionals in making better decisions.

The context in which this capability of Watson is one in which Watson is a resource to the financial services professional, simply a tool or resource they can use when advising clients. But it is not hard to envision a time when the clients could simply 'ask Watson' directly questions about their investing strategies and get information on anticipated outcomes. Why would we need, forever, an intermediary between us and the source of knowledge?

These are just a couple of quick examples I found in about 10 minutes of writing this piece this AM, but I bet there are plenty more out there (and more coming).

I guess my point is really that everyone, including bankers in expensive suits should be taking what is happening with robots and automation seriously. It's all fun and games until the algorithm can do your job better than you.

And who knows, maybe the next investment planning chart we will see in a few years will be titled 'Long Automated Advisors, Short Bankers'.

Have a great day!