The changing mix of employee compensation increases

Steve

SteveTL:DR - More and higher one-time bonuses, fewer and less annual salary/wage increases

In the aftermath of the recent tax reform legislation passed by the US Congress and signed by the President, you certainly must have noticed a pretty long list of major organizations who reacted to the reduction in the US corporate tax rate by (among other things), awarding bonuses (oddly, almost all exactly in the amount of $1,000) to their employees.

Here is just a short list of select companies who have shared this windfall with their employees in the form of one-time bonuses:

Alaska Air, American Airlines, AT&T, Bank of America, Comcast, Disney, Home Depot, Lowe's, Southwest Air, Walmart, Waste Management - and there are lots more.

The companies above, (and plenty others) have directed the employee rewards portion of their expected tax cut windfall to these one-time bonuses, while a few others (Aflac, Boeing, Cigna, FedEx, Honeywell, UPS, Visa), have either supplemented these one-time bonuses with other employee rewards improvements - increases hourly wages, 401(k) contribution enhancements, and/or stock-based rewards.

But the vast majority of publicly announced employee rewards increases as a result of the corporate tax cut have been these seemingly ubiquitous one-time $1,000 bonuses. It is almost odd, (and if you are a conspiracy lover, curious), that so many companies in different industries all settled on this same bonus amount. Weird...

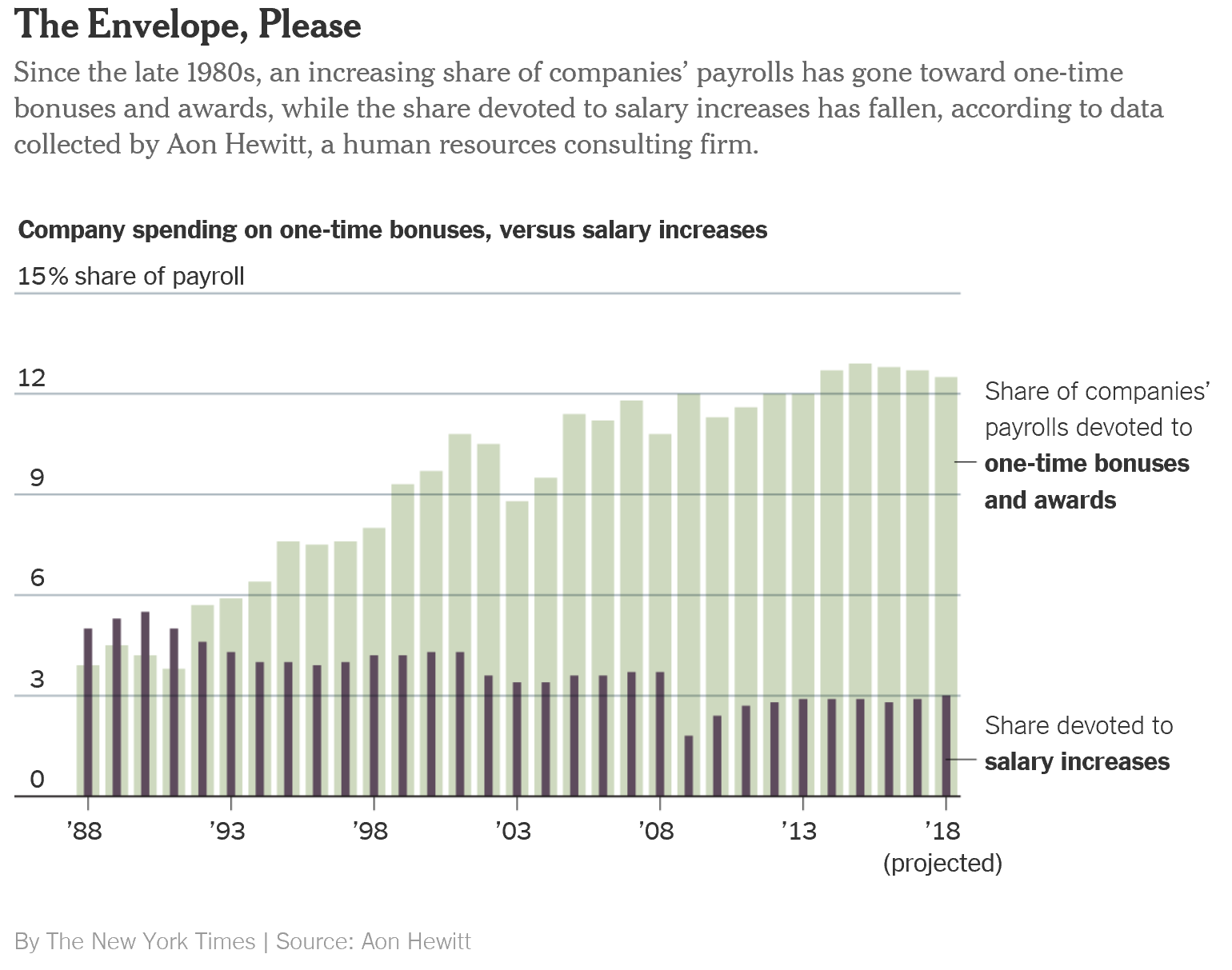

But these tax cut bonuses also draw our attention to a larger trend in employee compensation increases, one that pre-dates the recent surge in one-time tax cut bonuses - the trend of companies allocating more payroll budget towards one-time and variable awards, and relatively less budget to annual (and in theory, recurring), salary/wage increases. Said differently, more and more of the compensation increase that an average worker might see is tied up in discretionary and variable methods, like one-time bonuses. Check out this chart from a piece in the NY Times, reporting on an Aon Hewitt study of the topic:

Back in 1991, for example, variable pay (like one-time bonuses) took up about 3% of total compensation budgets, while the budget for annual salary increases was 5%.

Fast forward to 2017 and the amount of budget allocated to one-time bonuses has risen to 12.7% while the amount earmarked for annual salary increases has fallen to 2.9% (the 'getting 3%'ed to death phenomenon).

A closer look at the data shows that after taking an expected financial crisis/recession dive in 2008/2009, compensation budget allocations have not really recovered to their pre-recession levels, while the budget for one-time bonuses and awards has continued on a slow and steady climb. This makes sense for a few reasons. The harsh economic environment from the recession era is still on many CEO's minds, and the need to be more flexible and adaptable, (especially when it comes to employee compensation), has become standard operating procedure and many companies. E

Given these recent tax cut bonuses play into that line of thinking - CEOs can't be sure these tax cuts will be permanent, a change in control or philosophy of Congress could alter the landscape at almost any time. Giving one-time bonuses instead of 'permanent' salary/wage increases allows companies to respond to market, competitive, and economic conditions in almost real-time, whereas granting (and potentially removing), salary/wage increases is a much more difficult challenge to manage. Have you ever known any worker who will accept a salary or wage cut cheerfully?

But beyond that, companies still need to keep worker's desires in mind, after all the labor market remains extremely tight. The Times reports that a second Aon Hewitt survey showed that when asked what they wanted their companies to do with their tax cut windfall 65% of them said they wanted a pay raise, far more than other options like a bonus or an increase to the 401(K) contribution. Interesting stuff for sure.

Compensation is a tough job for sure. And oddly, it doesn't get that much easier when there are more dollars to spread around.

Have a great day!