Happy New Year!

To start 2019, I wanted to share a chart from and the link to the fascinating report titled 'From Insight to Action: JUST Capital's 2018 Survey Results & Roadmap for Corporate America'.

For those not familiar, Just Capital, is a nonprofit founded in 2013 by a group that includes billionaire investor Paul Tudor Jones, and who has conducted an annual survey since then to determine which corporate-behavior-issues the American public cares about the most. Just Capital then ranks 1,000 large companies based on their performance on those issues which the survey has shown the public is most concerned with. The rankings are also the basis for the Just U.S. Large Cap Equity ETF, which launched in June 2018.

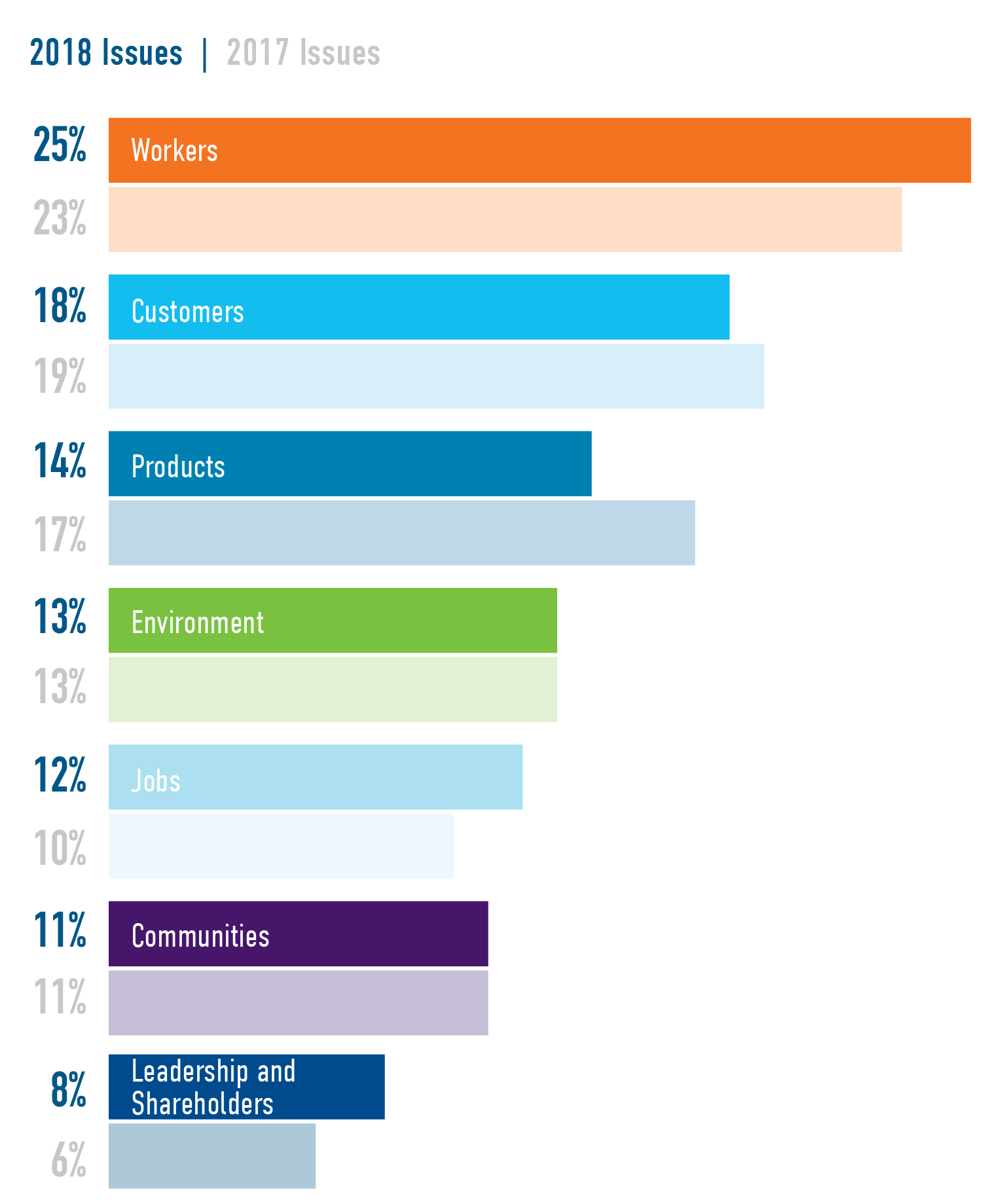

Of interest to HR folks, in these surveys, worker pay and benefits consistently rank at the top of respondents' priorities. Here's the chart, which shows which general category or issues, (workers, customers, environment, etc.), that survey respondents indicated where more or less important to them when assessing a company (and compared to the 2017 survey). Here's the chart, then some comments from me after the data.

Some quick observations from this data, which shows that the broad range of 'employee' issues are what the American public cares about the most when evaluating companies.

1. Concern for workers issues is trending up. In both the chart above, and in some underlying data from the report, Americans are increasingly concerned about worker's conditions, pay and benefits, and work/life balance issues. Perhaps this is the outcome of a 10-year run of an improving and tightening labor market that is leading individuals to be more open and assertive of what they look for in an employer and what they see as just treatment of workers by a company.

2. Shareholders may not be 'first' forever. Despite 'shareholders' seeming to be the ones to benefit the most in the last decade, the public cares about how companies treat shareholder and leadership issues the least. While millions of American workers are also shareholders of companies through retirement and other investments, most average employees see themselves in a different category than the large, institutional investor class. By this logic, if employee issues and concerns are going to be more important, shareholder concerns are seen as less important.

3. Creating a 'just' company for employees is not that complicated. The Top 3 underlying components that influence how the workplace treats employees are providing good benefits, paying a living wage, and providing a safe workplace. There were the elements ranked as most important to survey respondents, and quite honestly, seem to represent the lowest common denominator for employers to strive for. Said differently, it probably is not as hard as the experts make it out to be, to create a workplace that is just and fair for employees.

This is really interesting data, I encourage you to check out both the report and the Top 100 rankings according to Just Capital's survey of American workers. While there are quite a few companies on the list we frequently see on other 'Great' workplace type lists, there are also many other names you might not be as familiar with.

Have a great day and a happy, and successful 2019!

Steve

Steve