CHART OF THE DAY: What do employee health benefits cost anyway?

Steve

SteveIn between arguing with sports teams, players, owners, and fans on Twitter, one of the other things that the US government's leaders have spent a bunch of time on in 2017 are the attempts, (and so far, 'attempting' is all that has been done), at revising, reforming, or replacing the Affordable Care Act, aka Obamacare.

And while I, or no one else as far as I can tell, has any clue what is going to happen with the ACA and whatever might come next, I have been thinking about benefits, in particular employer sponsored health benefits lately, for reasons that are both boring and not really that important.

While on a internet foray on this topic over the weekend, (I know, my life is REALLY exciting), I landed on an excellent resource for this kind of data, Kaiser Family Foundation/Health Research & Educational Trust (HRET) 2017 Employer Health Benefits Survey, which was recently released.

The annual survey is a joint project of the Kaiser Family Foundation and the Health Research & Educational Trust. The survey was conducted between January and June of 2017 and included 3,938 randomly selected, non-federal public and private firms with three or more employees (including 2,137 that responded to the full survey and 1,801 others that responded to a single question about offering coverage).

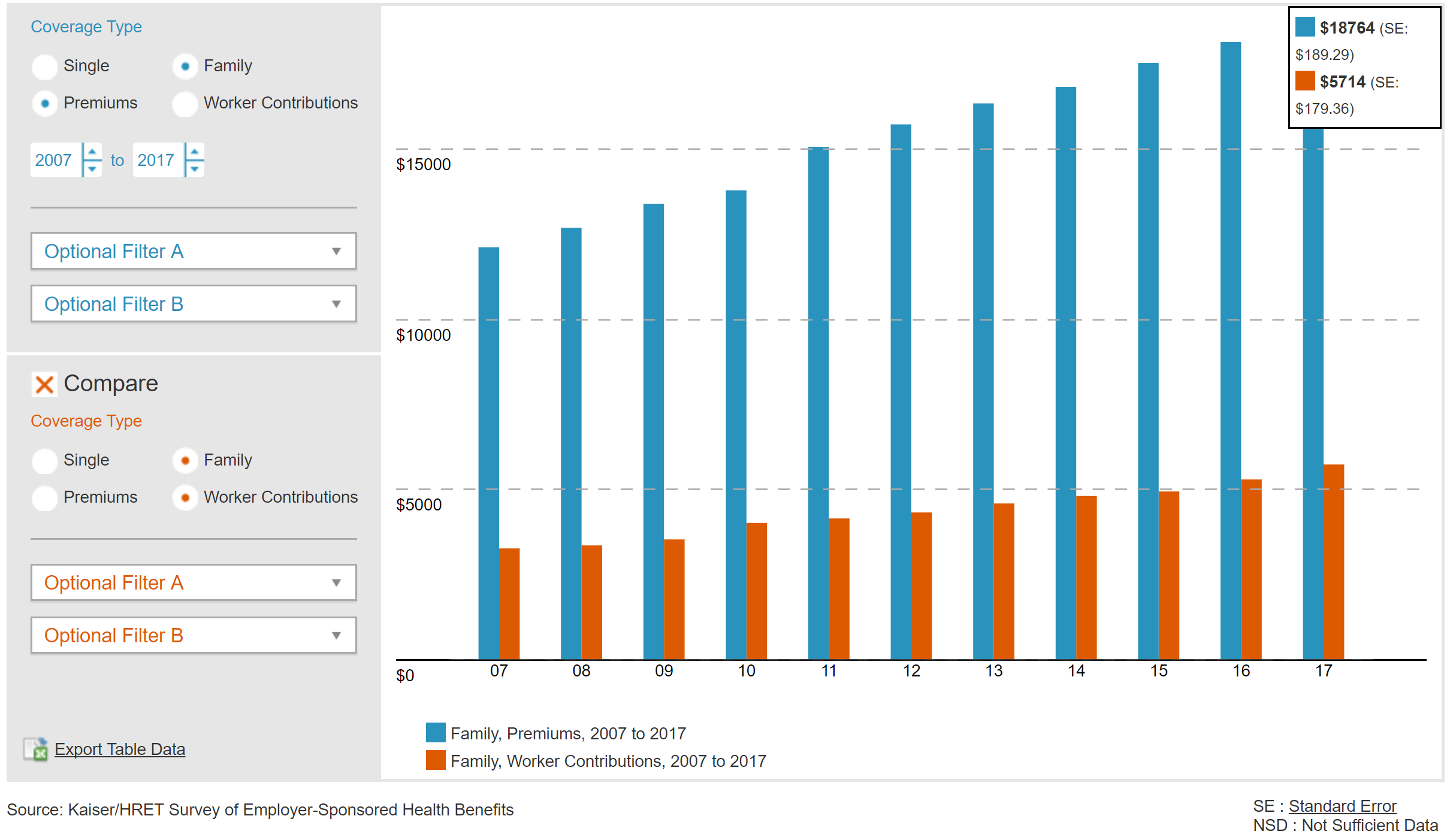

So to get back to the title/question of the post, here is today's CHART OF THE DAY, a quick look at just what employer sponsored health care benefits cost, (the premium) and how much the average employee contributes to that cost. Here's the data, then some comments from me after the chart:

Some thoughts...

1. Wow, that chart is harder to read than I hoped for. Here is a link to the  in a much larger size.

in a much larger size.

2. In case you still have trouble making out the details, for 2017 the average cost (premium) for employer-based family coverage was $18,764 annually with the employee contributing, on average, $5,714, or about 30% of the premium.

3. This split, or ratio of employer funding to employee contribution varies a bit by company size. According to Kaiser Family Foundation, companies larger than 200 employees contribute about 72% of the annual premium, while smaller employers (fewer than 200 employees), only contribute 64%. This difference equates to about an extra $1,600 annually that the employee would have to contribute.

4. Surprisingly, the rate of premium increases has slowed in recent years. According to the survey, annual family premiums for employer-sponsored health insurance rose an average of 3 percent to $18,764 this year, continuing a six-year run of relatively modest increases.

5. There are about 151 million Americans who are covered via an employer-sponsored healthcare plan. That makes the employer market by far the single largest source of health care coverage for folks in the US.

Really interesting data, and there is lots more to dig into at the KFF site.

As I said, I have no clue what is going to happen with ACA, or whatever might come next. But I do think the more you know about how many Americans access and pay for health care the better informed you will be and the better prepared to make decisions for yourself, your family, and your organization.