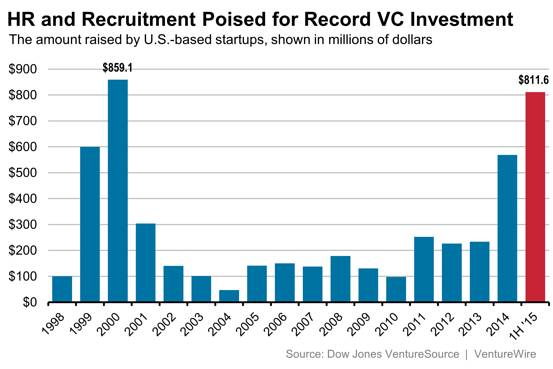

CHART OF THE DAY: Surging Investments in HR Tech

Steve

SteveReally a simple and self-explanatory Chart of the Day for a busy Tuesday, this one courtesy of the Wall St. Journal. Take a look at the chart of venture capital investment in the HR and Recruiting technology market from 1998 to the present, and as you expect and demand, some FREE commentary from me after the data.

Some quick takes:

1. First, to level set, the first half of 2015 with investment of about $811M is almost greater than the highest-ever yearly total of $859M back in 2000. Ah, 2000. The 'dot-com' era. Good times. But looking at the data you could argue that the HR tech market for VC investment really did not recover from the dot-com crash until very recently, like last year. So it could be that a prolonged period of under-investment is partially to account for the dramatic increases in 2014 and so far in 2015.

2. Let's go ahead and assume that most VCs have plenty of options and opportunities for investment. If that is the case, then this windfall of money flowing into the HR tech space is good news for a large array of industry players - folks who can sell HR tech solutions, marketers, analyst firms, HR conferences, and even little 'ol bloggers like me, who have lots of products to see, think about, and potentially write about. It is a sure sign of an industry that is primed for growth when the investment levels are surging upwards as we see in the WSJ. It's like the dot-com years all over again. At least let's hope we don't crash like we did from '02 - '04.

3. What does this mean for the really important players in the HR tech market - the actual customers? Well in the broadest strokes it is mostly positive. More investment creates more competition which leads to better products and more customer choices. And while sometimes it seems like in HR tech that the bigger, more established players have gobbled up via acquisition many of the new entrants, I can assure you that judging from the number of HR tech startup demos I have been doing that there is no shortage of new ideas and innovation in the space. This is a great time to be a customer of HR Tech, even if the market can be a little tricky to navigate.

But like I said, good times all around - for the VCs, for the startups, and most importantly, for the customers and HR leaders who have access to an ever-expanding set of tools and technologies to help them improve results in their organizations.